Zero-Trust SaaS for Canadian Business: OSFI B-13, FINTRAC & PIPEDA Compliance

1. The Compliance Gap That Is Costing Canadian Businesses

In January 2024, OSFI’s Guideline B-13 — Technology and Cyber Risk Management — came into force for all federally regulated financial institutions in Canada. The guideline, which had been in development since 2022, established enforceable expectations for how Canadian banks, insurance companies, credit unions, and trust companies must manage technology and cyber risk from the architecture level up [OSFI, 2024].

At roughly the same time, FINTRAC was intensifying its enforcement posture. In early 2024, TD Bank received a CAD $9.2 million administrative monetary penalty for compliance failures that included inadequate suspicious transaction reporting and insufficient continuous monitoring [Global Relay, 2025]. In the same year, FINTRAC issued penalties exceeding CAD $5 million against multiple FinTech firms for similar AML reporting failures [PayCompliance, 2025].

Meanwhile, Canada’s proposed federal cybersecurity legislation — originally Bill C-26, now reintroduced as Bill C-8 — continued its path toward mandatory cybersecurity programs and incident reporting requirements for operators of critical infrastructure, including the banking and finance sector [SecurityBrief Canada, 2026].

The picture that emerges is consistent: the Canadian regulatory environment is tightening, enforcement is increasing, and the cost of non-compliance is rising sharply. Yet a substantial portion of Canadian mid-market businesses in the regulated sector are still running their core operations on off-the-shelf platforms built for US or European compliance regimes — platforms that were not designed for OSFI B-13 compliance, FINTRAC AML obligations, or Canadian data sovereignty requirements.

The compliance gap is real. This guide — the definitive Canadian business guide to zero-trust SaaS — is designed to help you understand it and close it.

What you will learn in this guide:

- The four core principles of zero-trust architecture for Canadian financial services, explained for a regulated-sector context

- Which Canadian regulations apply to your sector and what they specifically require at the platform level

- How zero-trust SaaS maps to FinTech, HealthTech, and non-profit use cases

- Why off-the-shelf SaaS platforms consistently fail the Canadian regulated buyer

- How a compliance-first custom SaaS platform is actually built by a Canadian software vendor

- What to ask your current vendor to assess your real compliance exposure

Internal Resources:

- OSFI Cyber Risk Guidelines Explained for Software Vendors →

- How to Build Multi-Tenant SaaS for Canadian FinTech Startups →

- FINTRAC AML Compliance: What Your Software Needs to Do →

- Role-Based Access Control in Healthcare SaaS →

- Why Canadian Non-Profits Are Rethinking Donor Data Infrastructure →

- The Hidden Cost of Off-the-Shelf SaaS for Canadian Regulated Businesses →

2. What Zero-Trust Architecture Actually Means

Zero-trust is a security design philosophy, not a product you can purchase or enable in an admin panel. The model was formally defined by NIST in Special Publication 800-207 and has since been adopted by regulators and governments worldwide — including the Government of Canada’s own Shared Services Canada, which has made Zero-Trust Architecture (ZTA) a core principle of its Cyber Security Services Roadmap [Canada.ca, 2025].

The foundational premise of zero-trust architecture in Canada’s regulated sector: no user, device, or system is automatically trusted — not even those inside your corporate network. Every access request must be authenticated, authorised, and continuously verified before it is granted.

Canada.ca describes ZTA as a security framework focused on protecting infrastructure and data where “subjects in a system should not be trusted by default” — including applications, users, and devices.

In the context of Canadian regulated SaaS platforms, this matters because the primary attack vectors are not dramatic external breaches — they are credential theft, insider threats, misconfigured access controls, and lateral movement following a partial compromise. Traditional perimeter security, which trusts everything inside the network, is structurally unable to contain these threats.

The Four Core Principles of Zero-Trust for Canadian Financial Services

Principle 1 — Never Trust, Always Verify

Every request — whether it originates inside or outside the network perimeter — is treated as potentially hostile until verified. Authentication is not a one-time event at login; it is a continuous process evaluated against identity, device posture, location, behavioural context, and time of access. For a Canadian FinTech platform processing Interac transactions, this means that a user who authenticated this morning does not automatically retain that trust at 2:00 AM if their access pattern changes.

Principle 2 — Least-Privilege Access

Users and systems receive only the minimum permissions required to perform their specific function. A loan officer who needs to view an applicant’s credit assessment should not have access to the core banking ledger. A junior developer who needs to debug a payment API should not have database administrator privileges. Over-privileged accounts are one of the most common enablers of catastrophic data breaches — and one of the most common findings in OSFI audit reviews of financial institution access management.

OSFI’s Guideline B-13 explicitly requires that FRFIs implement Privileged Access Management (PAM) controls. Platforms that cannot enforce least-privilege at the code level — where access is defined in the application architecture, not just in an external configuration file — are architecturally non-compliant with OSFI B-13.

Principle 3 — Micro-Segmentation

Rather than defending a single network perimeter, zero-trust divides network and application layers into small, isolated zones. A compromise in one segment cannot propagate laterally to another. For a Mobile Financial Services (MFS) platform handling millions of daily transactions, micro-segmentation is the difference between an isolated incident and a systemwide breach. For a Canadian HealthTech SaaS platform serving multiple hospital clients, it is the architectural control that prevents one tenant’s data from being accessible by another tenant’s breach.

Principle 4 — Assume Breach

Zero-trust systems are designed with the assumption that a breach has already occurred or is currently in progress. This drives continuous monitoring, immutable audit logs, rapid isolation capabilities, and incident response workflows that do not depend on detecting the initial point of entry. For Canadian regulated businesses, this principle directly maps to OSFI’s requirement for cyber resilience — the ability to absorb, contain, and recover from a cyber incident without catastrophic operational failure.

Zero-Trust vs. Traditional Perimeter Security

| Dimension | Traditional Perimeter Security | Zero-Trust Architecture |

|---|---|---|

| Trust Model | Trust anything inside the network | Never trust, always verify every request |

| Access Control | Broad access once inside the perimeter | Least-privilege; access scoped to task |

| Breach Assumption | Focused on keeping attackers out | Assumes breach; limits blast radius |

| Monitoring | Perimeter alerts only | Continuous verification across all layers |

| OSFI B-13 Alignment | Does not meet B-13 expectations for IAM and PAM | Fully aligned with OSFI B-13 principles |

| PIPEDA Compliance | No inherent data minimisation or audit trail | Supports data minimisation and full audit logging by design |

3. The Canadian Regulatory Landscape

This section covers the specific regulations that apply to regulated-sector SaaS in Canada. Generic IT compliance content stops here and Canadian compliance reality begins. The ability to name these regulations, cite their specific requirements, and explain how platform architecture maps to them is the core of what separates a compliant Canadian SaaS platform from a generic one.

Note for vendors: If your software is used by a federally regulated financial institution, healthcare organisation, or government-funded non-profit, the regulations below apply to your platform — even if you are not the regulated entity. Your clients’ auditors will ask about your platform’s compliance architecture.

OSFI Guideline B-13 — Technology and Cyber Risk Management

What it is: OSFI’s Guideline B-13 is the primary technology and cyber risk framework for all federally regulated financial institutions (FRFIs) in Canada — banks, insurance companies, trust companies, pension plans, and cooperatives. It came into force on January 1, 2024, having been finalised in July 2022.

Why OSFI B-13 compliance matters for software vendors: As Torys LLP notes, B-13 establishes OSFI’s expectations for how FRFIs should manage technology and cyber risk, defining it as a “comprehensive, enterprise-wide exercise at both technical and governance levels.” Critically, this includes technology procured from third-party vendors. If your platform is used by a FRFI, it sits within their B-13 compliance scope — making OSFI B-13 compliance software a direct procurement requirement.

Key requirements with platform implications:

- Governance (Principle 1 of B-13): Senior management must be assigned responsibility for technology and cyber risk. Platforms must generate governance-level reporting — risk dashboards, exception reports, access anomaly summaries — that FRFI boards and C-suite can review.

- IAM and PAM (Principles in B-13’s Cyber Security domain): FRFIs must implement Identity and Access Management controls, including Multi-Factor Authentication and Privileged Access Management. OSFI’s B-13 self-assessment tool confirms that platforms must support continuous monitoring and verification of privileged user sessions.

- SDLC Security (Principle 4): Norton Rose Fulbright notes that B-13 requires FRFIs to implement SDLC processes that “achieve security and functionality” — with documented control gates at each stage. For software vendors, this means your development pipeline — CI/CD, SAST, DAST — must be documented and demonstrable.

- Annual VAPT: At minimum, one annual Vulnerability Assessment and Penetration Test is required for systems handling regulated data. The VAPT report must be available for OSFI inspection.

- Incident Reporting: FRFIs must notify OSFI whenever a reportable technology or cybersecurity incident occurs. Platforms must support rapid isolation, forensic logging, and documented incident response workflows.

OSFI B-13 and companion guidelines: B-13 is read alongside Guideline B-10 (Third-Party Risk Management), which came into effect May 1, 2024, and applies specifically when technology risk is managed by a third-party vendor. Torys LLP notes that B-10 “will apply when the technology asset comes from, or the technology and cyber risk is being managed by, a third-party vendor for the FRFI.”

Official Reference: OSFI Guideline B-13 — Technology and Cyber Risk Management

FINTRAC — PCMLTFA and AML Compliance

What it is: The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) is Canada’s financial intelligence unit, administering the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA). Any platform touching Canadian financial transactions — payment processors, lending platforms, digital wallets, money services businesses — operates under FINTRAC’s oversight. A FINTRAC AML compliance platform is no longer optional infrastructure; it is a legal requirement.

Why enforcement is intensifying: In 2024, FINTRAC imposed a $9.2 million administrative monetary penalty on TD Bank for non-compliance with the PCMLTFA, with violations including failures to report suspicious transactions and inadequate continuous monitoring. The message was clear: FINTRAC will pursue enforcement regardless of institutional size.

2024–2025 regulatory expansion: FINTRAC’s latest directives significantly expanded the scope of reporting entities. As of April 1, 2025, financing and leasing companies, factoring companies, and cheque-cashing companies became reporting entities. New obligations came into force October 1, 2025, including requirements for beneficial ownership transparency reporting.

Key platform requirements:

- Suspicious Transaction Reporting (STR): Platforms must identify and report suspicious transactions more proactively, including transactions linked to virtual assets and high-risk jurisdictions. STR workflows must be built into the platform architecture, not managed through manual processes.

- Large Cash Transaction Reports (LCTR): Automated detection of transactions over $10,000 is required. Virtual currency transactions exceeding CAD $10,000 now require LCTR reporting, aligning with FATF recommendations.

- Record-Keeping: MSBs and PSPs must maintain detailed transaction logs, including customer identification and risk assessments, for at least five years. Records must be producible to FINTRAC within 30 days upon request.

- Beneficial Ownership: New FINTRAC obligations require reporting entities to report material discrepancies between their records and a company’s beneficial ownership registry filings where there is a high risk of money laundering or terrorist financing.

Canada preparing for FATF evaluation: Canada is preparing for an evaluation by the Financial Action Task Force (FATF) scheduled for 2025-2026, which could prompt further regulatory adjustments to meet international AML standards. Platforms built today should anticipate further tightening.

Enforcement context: Under the Strong Borders Act, cumulative penalties for multiple FINTRAC violations will be capped at CAD $20 million or 3% of global revenue — whichever is greater — applied at the group level for affiliated entities. For large Canadian reporting entities, this 3% cap could result in penalty ceilings exceeding $1 billion.

Official Reference: FINTRAC Obligations and Guidance

PIPEDA — Personal Information Protection and Electronic Documents Act

What it is: Canada’s federal private-sector privacy law. PIPEDA applies to any organisation collecting, using, or disclosing personal information in the course of commercial activities — including most FinTech and HealthTech platforms. PIPEDA compliant SaaS is a baseline expectation for any platform handling Canadian consumer data.

Current status and trajectory: The European Commission’s 2024 review confirmed that PIPEDA continues to offer an adequate level of protection relative to EU GDPR, but flagged areas for improvement, signalling that Canada’s privacy framework faces continued external scrutiny.

Canada’s proposed replacement for PIPEDA — the Consumer Privacy Protection Act (CPPA) under Bill C-27 — died on the order paper in January 2025. The new federal government has signalled a replacement statute is expected to be introduced, potentially with fines of up to the greater of CAD $25 million or 5% of gross global revenue.

Key platform implications:

- Breach notification: Under PIPEDA Section 10.1(1), organisations must report breaches to the OPC as soon as feasible where there is a real risk of significant harm. In 2024-2025, the OPC received 693 PIPEDA breach reports — a 28% increase over the prior year — with breach reports continuing to rise in the first half of 2025.

- Data sovereignty: Canada’s open banking framework and the Consumer-Driven Banking Act create data portability and security safeguard requirements. Complementary PIPEDA amendments are expected in 2026 to operationalise the data mobility framework, with regulations setting out security safeguards for the permission-based sharing of financial data.

- Provincial privacy law: Organisations operating in Quebec are subject to Law 25, British Columbia operations are covered by PIPA, and Ontario health data is governed by PHIPA. Each has specific requirements that differ from federal PIPEDA requirements.

Official Reference: Office of the Privacy Commissioner — PIPEDA Overview

Bill C-8 (formerly Bill C-26) — Critical Cyber Systems Protection

What it is: Canada’s proposed cybersecurity legislation for critical infrastructure, including the banking and finance sector. Originally introduced as Bill C-26 in 2022, it passed the House of Commons in June 2024, died on prorogation in January 2025, and was reintroduced as Bill C-8 in June 2025. As of early 2026, C-8 is progressing through the Standing Committee on Public Safety and National Security.

Why it matters now: Even in its unpassaged form, Bill C-8 signals the direction of Canadian cybersecurity compliance for software vendors. Platforms being built today for 5+ year deployment cycles should be architected to accommodate its requirements:

- Mandatory cybersecurity programs for designated operators

- Supply chain and third-party risk mitigation requirements

- Mandatory incident reporting above prescribed thresholds

- Government power to compel action in response to identified threats

Related Reading: Espace Info Tech on Canadian cybersecurity compliance →

Health Canada — Data Standards for HealthTech Platforms

Health Canada governs traceability and data standards for software handling patient records, drug dispensing data, and clinical trial information.

Key requirements:

- PHIPA (Ontario): Role-Based Access Control (RBAC) for patient records is a compliance requirement. Every access event on patient health information must generate an audit log entry. Patients have the right to access their own audit trail in certain circumstances.

- Quebec’s Law 25: Applies to non-profits and healthcare organisations operating in Quebec. Requires data minimisation, a privacy impact assessment process, a documented data processing register, and a mandatory Privacy Officer designation.

- BC’s PIPA and other provincial acts: Each province has its own health privacy legislation with specific requirements that differ from PHIPA. A national HealthTech platform must comply with all applicable provincial regimes simultaneously.

4. Zero-Trust by Sector: What It Looks Like in Practice

FinTech and Mobile Financial Services Platforms

Related In-Depth Guide: How to Build Multi-Tenant SaaS for Canadian FinTech Startups →

| Security Layer | Zero-Trust Implementation | Regulatory Driver |

|---|---|---|

| Identity Verification | Multi-factor authentication, device posture checks, continuous session re-validation | OSFI B-13 IAM expectations |

| Transaction Monitoring | Real-time anomaly detection calibrated to FINTRAC risk thresholds; automated STR/CTR workflows | FINTRAC PCMLTFA |

| API Gateway Security | OAuth 2.0, signed request verification, rate limiting per tenant for interface and open banking APIs | Consumer-Driven Banking Act (CDS APIs) |

| KYC and Identity | Canadian-certified identity verification services, document retention per FINTRAC schedule | FINTRAC record-keeping requirements |

| Beneficial Ownership | UBO verification workflows, discrepancy reporting to federal registry | FINTRAC October 2025 amendments |

| Audit Logging | Immutable, tamper-evident logs; 5-year retention; producible within 30 days on request | FINTRAC record-keeping, OSFI B-13 |

| VAPT | Pre-deployment and annual VAPT with full report available for OSFI/FINTRAC review | OSFI B-13, PCI DSS |

| Incident Response | Documented escalation and notification workflows; OSFI-reportable incident classification | OSFI B-13, E-21 (incident reporting) |

The Interac Integration Challenge

Standard off-the-shelf SaaS platforms are not built for Canadian payment infrastructure. Interac’s Direct Payment and e-Transfer APIs require certified integrations with specific authentication and request signing requirements. Platforms attempting to bridge this gap with middleware add complexity, cost, and a new point of potential compliance failure. A custom zero-trust SaaS platform built for the Canadian FinTech market has these integrations designed in from the start.

HealthTech Platforms

Related In-Depth Guide: Role-Based Access Control in Healthcare SaaS →

| Security Layer | Zero-Trust Implementation | Regulatory Driver |

|---|---|---|

| Role-Based Access Control | Clinician (treating), clinician (consulting), admin, pharmacist, auditor roles — each with scoped data access | PHIPA; Health Canada data standards |

| Episode-Based Access | Access scoped to care episode duration; automatic revocation at episode close | PHIPA “need to know” access requirement |

| Break-Glass Access | Emergency override with mandatory justification and immediate privacy officer notification; post-hoc review queue | PHIPA; Health Canada traceability |

| Data Segregation | Patient data isolated by facility with encrypted inter-tenant boundaries | PHIPA; provincial privacy acts |

| Audit Logging | Every access event logged with user ID, patient ID, record type, clinical justification, and timestamp | PHIPA Section 12; Health Canada traceability |

| Breach Response | Automated isolation with PHIPA-compliant notification workflows to patients and privacy regulator | PHIPA; PIPEDA breach notification |

| Data Residency | Patient data stored on Canadian infrastructure; no foreign replication | PHIPA; Law 25 in Quebec |

NGOs, Non-Profits, and INGOs Platforms

Related In-Depth Guide: Why Canadian Non-Profits Are Rethinking Their Donor Data Infrastructure →

| Security Layer | Zero-Trust Implementation | Regulatory Driver |

|---|---|---|

| Donor Data Segregation | Multi-tenant architecture isolating each program’s donor and grant records | PIPEDA; Law 25; granting body requirements |

| Fund-Tracking Integrity | Cryptographic audit trails for fund disbursement — donor-auditable and grantor-auditable | Government grant compliance; CRA requirements |

| Access Governance | Least-privilege access: field workers, program staff, finance, and HQ each with scoped access | PIPEDA; provincial privacy acts |

| Data Residency | All data stored on Canadian infrastructure for government-funded operations | Federal and provincial grant requirements |

| Breach Notification | PIPEDA-compliant breach notification workflows with Privacy Officer escalation | PIPEDA Section 10.1; Law 25 (Quebec) |

5. The Build vs. Buy Trap

Related In-Depth Guide: The Hidden Cost of Off-the-Shelf SaaS for Canadian Regulated Businesses →

The most common objection from Canadian mid-market buyers: “Why not use Salesforce, SAP, or another established SaaS platform?”

It is a reasonable question. The answer is not that off-the-shelf platforms are bad — it is that they were not built for the specific compliance requirements of the Canadian regulated sector. The gap between what these platforms provide and what OSFI B-13 compliance, FINTRAC PCMLTFA, and Canadian provincial privacy law actually require is filled with middleware, manual processes, and compliance workarounds that consistently cost more than a purpose-built, custom SaaS solution over a 3-year horizon.

| Criterion | Off-the-Shelf ERP Software (SAP, etc.) | Custom ERP by Espace InfoTech |

|---|---|---|

| Canadian Tax & Compliance | Built around enterprise systems by default. General taxes (HST/GST) and provincial rules often require expensive third-party plugins. | Designed from day one for Canadian tax compliance (GST/HST, province-specific rules), reducing costly localization for manufacturing operations. |

| Cost & Total ROI | Annual licenses, consulting fees, and heavy implementation costs. Often exceeds ROI for mid-sized manufacturers. | Full ownership model suitable for SMEs—lower annual recurring costs, higher ROI over the medium term. |

| Industry-Specific Flexibility | Not built for Canadian operational workflows (production planning, quality controls). | Purpose-built for manufacturing workflows with modules aligned to Canadian operational benchmarks. |

| ITAR/CMMC & Export Compliance | Generalized tools require additional customization, but are less aligned with regulatory standards. | Well-structured and built with security controls aligned to compliance requirements of regulated industries. |

| TLIP Readiness | Vendor modules including warehouse, TLIP readiness may require customization for local ecosystems. | TLIP modules designed per shipping and inventory efficiency needs, reducing workflow friction. |

| OEE + IIoT Fit | Retrofitted sensor management at the enterprise level. Great overall flexibility, but less direct shop-floor usability. | Built architecture designed to directly support OEE + shop-floor operations. |

| ISO 9001 / ISO 27001 | Platform may be certified; your operational adaptation may still lag. | Built process design aligned around ISO 9001, ISO 27001, and OEE modules. |

| PME / Lean 5S | Generic project management tools may not serve Canadian Lean 5S requirements. | PME + workflow design aligned for PMO/Lean 5S and operational productivity. |

| Total Cost of Ownership (TCO) | Recurring customization + additional integrations = expensive TCO over time. | No per-seat licensing. Full ownership lets scaling fit evolving operational needs. |

| Regulatory Audit Support | Compliance add-ons may help, but often require manual audit workflows. | Client-centric audit logs, workflow documentation, and KPI reports built-in for compliance. |

The audit question to ask your current vendor right now:

“Can you provide us with a complete, immutable audit log of all data access events on our account for the last 12 months, in a format suitable for submission to OSFI or FINTRAC — without our developers’ involvement?”

If your Canadian SaaS vendor cannot do this quickly and cleanly, you have already found your first compliance gap.

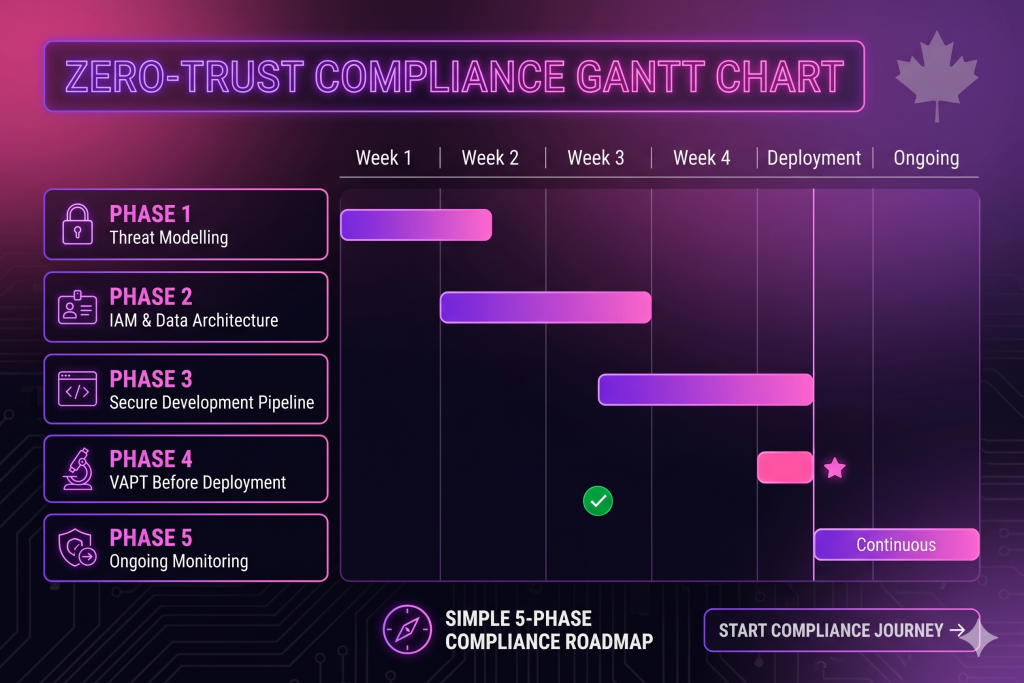

6. Zero-Trust in Practice: How Espace Info Tech Builds It

A zero-trust SaaS platform for the Canadian regulated sector is not a product you configure — it is an architectural commitment built across five phases by a Canadian software vendor with direct experience under OSFI, FINTRAC, and Canadian privacy law.

Learn more about Espace Info Tech’s full service offering at espaceinfotech.com

Phase 1 — Threat Modelling and Regulatory Mapping (Week 1–2)

Before a line of code is written, we model the threat landscape specific to your sector, regulatory obligations, and existing infrastructure. This phase produces:

- A Crown Jewels inventory — the specific data assets that, if compromised, would trigger a regulatory incident or significant harm. This mapping is a direct input to OSFI B-13’s requirement for institutions to have visibility into their critical assets.

- A Regulatory Obligation Map — which FINTRAC, OSFI, PIPEDA, and provincial requirements apply to this platform, cross-referenced with specific platform components.

- A Threat Actor Profile — the actors most likely to target your platform (organised financial crime for FinTech, healthcare record theft for HealthTech, grant fraud for NGOs) and their most likely methods.

Phase 2 — IAM and Data Architecture Design (Week 2–4)

Identity and Access Management is the backbone of zero-trust. We design the complete IAM architecture before the application layer is built:

- Authentication flows: MFA, SSO, certificate-based authentication, and session token expiry aligned with OSFI B-13 requirements.

- Authorisation models: RBAC for role-defined access (standard for HealthTech and NGO platforms); ABAC (Attribute-Based Access Control) for more granular transaction-level controls in FinTech platforms.

- Privileged Access Management (PAM): Time-limited elevated access with justification requirements, session recording, and independent logging — designed to satisfy OSFI B-13 PAM expectations.

- Data residency architecture: Multi-tenant isolation model (typically isolated database per regulated tenant), Canadian cloud region configuration, and documentation package for compliance evidence.

- Immutable audit log design: Write-only log store, separate from the application layer, with access controls independent of application administrators — meeting FINTRAC’s immutable audit log standard.

Phase 3 — Secure Development Pipeline (Week 4–Deployment)

Security is embedded in the development pipeline, not bolted on at release:

- SAST (Static Application Security Testing): Automated security analysis on every code commit. Vulnerabilities are caught in development, not in production.

- DAST (Dynamic Application Security Testing): Runtime security testing against the running application, executed on every build that reaches the staging environment.

- Security regression testing: A defined suite of security test cases that must pass before any deployment — preventing regression to known-insecure states.

- SDLC documentation: Every phase of the development lifecycle is documented with control gates — the documentation package required by OSFI B-13’s SDLC expectations.

Phase 4 — VAPT Before Deployment (Pre-Go-Live)

No platform leaves our delivery pipeline without a full Vulnerability Assessment and Penetration Test:

- External network and application layer penetration testing

- For multi-tenant platforms: tenant isolation testing — specifically verifying that a compromised tenant cannot access another tenant’s data

- API security testing including Interac and open banking integration endpoints

- A complete VAPT report, formatted for presentation to OSFI, FINTRAC, or healthcare compliance reviewers

The VAPT report is your property. You can submit it directly to regulators. You do not need to route it through us.

Phase 5 — Ongoing Monitoring and Compliance Maintenance

Delivery does not end at go-live:

- Continuous monitoring with automated alerting for anomalous access patterns, failed authentication spikes, and transaction volume anomalies

- Documented incident response runbooks calibrated to OSFI reportable incident thresholds

- Annual VAPT scheduling and execution

- Regulatory update monitoring — when OSFI, FINTRAC, or privacy regulators update their guidance, we proactively assess impact on your platform architecture

Book a 30-minute architecture review with Espace Info Tech →

7. What a Typical Engagement Looks Like

Case Study A — Canadian Credit Union (FinTech)

A Canadian credit union serving approximately 50,000 members needed to replace a legacy core banking interface that could no longer meet OSFI’s updated Identity and Access Management requirements under Guideline B-13. Specific requirements included:

- Interac Direct Payment and e-Transfer integration with immutable transaction logging

- RBAC for teller, branch manager, and administrator roles with full PAM controls

- A complete VAPT report for their annual OSFI B-13 review

- Deployment on Canadian cloud infrastructure to satisfy their board’s data sovereignty policy

Espace Info Tech delivered a custom zero-trust SaaS platform on Canadian infrastructure within six months. The client submitted a complete VAPT report and full IAM architecture diagram to their OSFI review. Their compliance team described it as the most complete OSFI B-13 compliance evidence package they had ever produced.

Client details anonymised at client request.

Case Study B — Canadian HealthTech Organisation (HealthTech)

A provincial HealthTech provider operating across multiple clinic locations needed a patient data platform that could satisfy both PHIPA (Ontario) and Health Canada’s traceability requirements, while providing mobile access for clinicians in field settings.

Key architecture challenges:

- Episode-based RBAC that would automatically revoke access when a care episode closed

- Break-glass access with mandatory justification logging and privacy officer notification

- Multi-facility data isolation — one location’s data must be completely inaccessible to other location’s staff

- Audit trail accessible to the privacy officer without developer support

The resulting PHIPA-compliant SaaS platform has since passed two provincial privacy commissioner reviews without finding.

Client details anonymised at client request.

8. Next Steps and Resources

The compliance gap in Canadian regulated-sector SaaS is real, widening, and increasingly expensive to ignore. OSFI B-13 is in force. FINTRAC enforcement is intensifying. Provincial privacy regulators are more active than at any point in the past decade. And Bill C-8 is progressing toward mandatory cybersecurity programs for critical infrastructure operators.

Generic platforms built for US or European markets cannot close this gap — not at the code level, not at the infrastructure level, and not in the audit trail. Canadian businesses in regulated sectors need a Canadian software vendor that builds for OSFI, FINTRAC, and Canadian data sovereignty requirements from day one.

Cluster Post Series — Go Deeper on Your Specific Topic

- C1 — OSFI Cyber Risk Guidelines Explained for Software Vendors → (Target: Compliance managers, bank IT heads)

- C2 — How to Build Multi-Tenant SaaS for Canadian FinTech Startups → (Target: CTOs, architects)

- C3 — FINTRAC AML Compliance: What Your Software Needs to Do in 2025 → (Target: Compliance officers, MFS operators)

- C4 — Role-Based Access Control in Healthcare SaaS → (Target: Hospital IT managers, HealthTech CTOs)

- C5 — Why Canadian Non-Profits Are Rethinking Donor Data Infrastructure → (Target: INGO procurement leads)

- C6 — The Hidden Cost of Off-the-Shelf SaaS for Canadian Regulated Businesses → (Target: CFOs, decision-makers)

Official Regulatory References (Backlink Targets)

These are the primary sources cited throughout this guide. We link to them directly to support topical authority and provide verifiable references for compliance teams:

- OSFI — Technology and Cyber Risk Management (Guideline B-13)

- OSFI — B-13 Self-Assessment Tool

- FINTRAC — Obligations and Guidance

- FINTRAC — Modernization and Upcoming Changes

- Office of the Privacy Commissioner — PIPEDA

- Canada.ca — Zero-Trust Architecture

- NIST SP 800-207 — Zero Trust Architecture

Ready to Assess Your Compliance Gap?

Download the Espace InfoTech Zero-Trust SaaS Compliance Checklist for Canadian Regulated Businesses — a regulation-referenced checklist covering OSFI B-13, FINTRAC PCMLTFA, PIPEDA, and Health Canada requirements. Use it to evaluate your current platform or scope a new build.

Or book directly: 30-minute architecture review with Espace Info Tech →

We will map your regulatory obligations to your current architecture and tell you honestly where the risks are.

Espace Info Tech Ltd is a Canadian custom software development firm specialising in Zero-Trust SaaS platforms for the regulated sector. We build for FinTech, HealthTech, and non-profit organisations operating under OSFI, FINTRAC, PIPEDA, and Health Canada requirements. Visit us at espaceinfotech.com →

Regulatory Disclaimer: This article is intended for informational purposes and does not constitute legal advice. Regulatory requirements change — always consult the official regulatory sources linked throughout this article and seek qualified legal counsel for your specific compliance obligations.