FINTRAC AML Compliance: What Your Software Needs to Do in 2025

FINTRAC has updated its expectations for 2025. Does your platform reflect these changes? Currently, the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) is intensifying its oversight of the digital economy. Any platform handling Canadian transactions—payment processors, digital wallets, or lending sites—operates under its strict scrutiny.

Regulatory expectations are shifting rapidly. Consequently, software built to 2020 standards is likely obsolete. To remain competitive, your stack must evolve to meet modern FINTRAC AML compliance software 2025 standards.

What FINTRAC Requires at the Platform Level

FINTRAC regulates Reporting Entities (REs), not the software itself. However, your platform is either an asset or a major liability for these entities. If your software fails to flag a suspicious transaction, your clients face heavy enforcement. As a result, you risk losing your market share and your reputation.

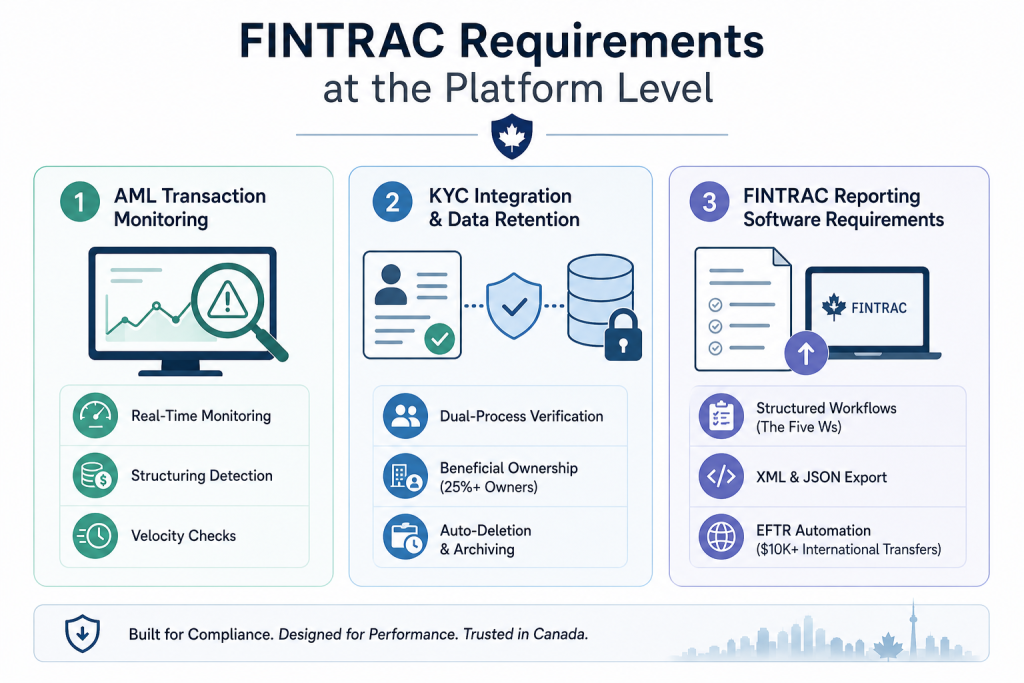

1. AML Transaction Monitoring Canada: The Real-Time Mandate

Modern AML transaction monitoring Canada protocols require more than simple threshold checks. In 2025, the focus has shifted toward behavioral patterns and velocity.

Real-Time Logic: High-volume platforms cannot rely on batch processing. Instead, your logic must evaluate transactions as they occur. If a user attempts to move funds, the system must check for risk before the transaction completes.

Structuring Detection: Implement automated rules to flag “structuring.” This involves users making multiple small transactions to stay below the $\$10,000$ reporting threshold. Furthermore, your system should track these attempts across multiple days and accounts.

Velocity Checks: Consequently, your architecture needs a high-performance caching layer (like Redis) to track transaction frequency without slowing down the user experience.

2. KYC Integration and Data Retention

You must verify identities before processing a single dollar. Therefore, your platform needs seamless integration with Canadian-certified identity services.

The Dual-Process Method: Ensure your platform supports the “dual-process” method. This involves verifying a user’s name and address against two different, reliable sources.

Beneficial Ownership: In 2025, you must do more than verify the business entity. Your software must collect and verify the owners of corporate clients. Specifically, anyone owning $25\%$ or more must be identified.

When a compliance officer identifies a suspicious event, a simple note in a CRM is insufficient. Your platform must follow specific FINTRAC reporting software requirements to remain viable in the Canadian market.

Structured Workflows: Your system must guide users through the reporting process. It should capture the “Five Ws”: Who, what, when, where, and why.

XML and JSON Export: Ensure your system can export data in the exact formats required by FINTRAC’s API or reporting portal. Manual data entry is a recipe for error. Therefore, automated schema mapping is essential.

Electronic Funds Transfer Reports (EFTRs): Any international transfer of $\$10,000$ or more must be reported within five working days. Your software should automate this flagging process to prevent late filings.

Immutable Audit Trails: The Non-Negotiable

FINTRAC inspectors can demand access to your records at any time. Consequently, your audit trails must be immutable.

Standard database logging is often insufficient. For example, administrators can technically delete entries to hide errors. Instead, implement a “write-once, read-many” (WORM) storage strategy. Use a separate, append-only environment with independent access controls. This ensures that even if an application server is compromised, the evidence remains intact. This is a core pillar of OSFI technology risk management Canada protocols.

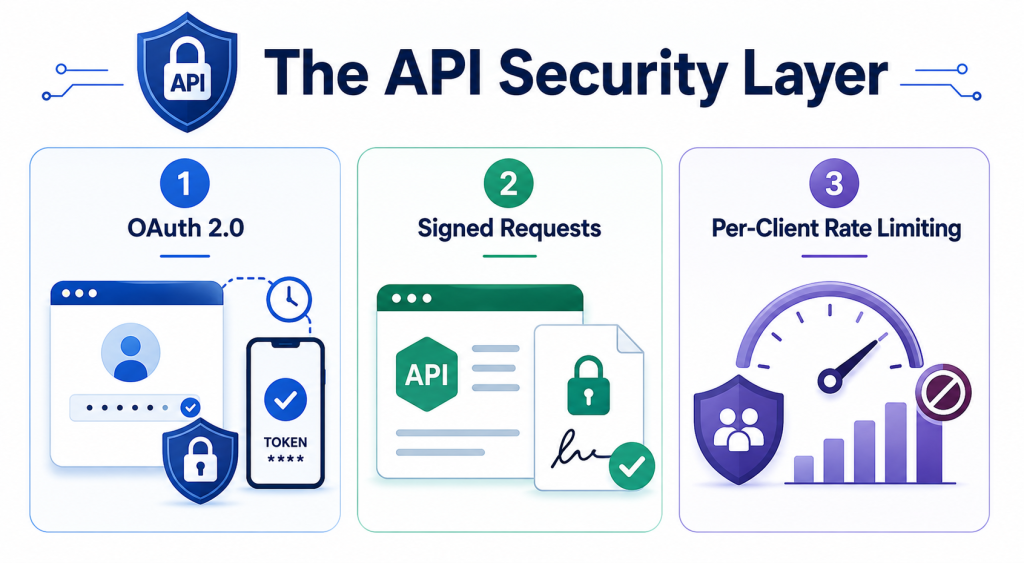

The API Security Layer

Security is now a compliance issue. A compromised API that allows data manipulation is a direct regulatory violation. To protect your integrity, implement:

OAuth 2.0: Use short-lived tokens for all integrations to minimize the window of attack.

Signed Requests: Verify that transaction data has not been modified in transit. This is critical for preventing “Man-in-the-Middle” attacks on financial data.

Per-Client Rate Limiting: This prevents automated manipulation and “brute-force” transaction attempts. Furthermore, it protects your system’s availability during high-traffic events.

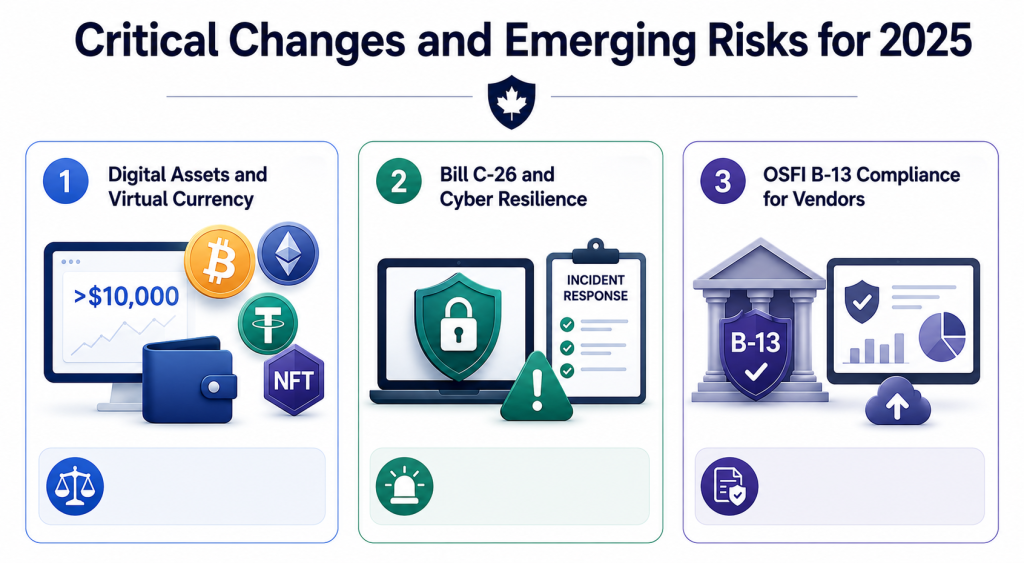

Critical Changes and Emerging Risks for 2025

The legislative framework in Canada is evolving. To build Canadian financial regulation software, you must anticipate these three shifts:

Digital Assets and Virtual Currency

Virtual currency transactions over $\$10,000$ are now subject to the same LCTR rules as cash. Whether you handle Bitcoin, Stablecoins, or NFTs, the compliance logic must be identical to fiat currency.

Bill C-26 and Cyber Resilience

This proposed law will mandate cybersecurity incident reporting for financial platforms. Consequently, your software must have built-in “Incident Response” modules. These modules should log breaches and facilitate the reporting process to the relevant authorities.

OSFI B-13 Compliance for Vendors

If you provide SaaS to a Canadian bank, you must meet OSFI B-13 compliance for vendors. This means proving your platform has robust threat detection and recovery capabilities. Furthermore, you must provide regular reports on your “security posture.”

Building for the Future

Building for compliance is a journey, not a destination. Don’t wait for an audit to find the gaps in your architecture. Shortcuts taken today will inevitably lead to regulatory hurdles that could tank your Series A or B funding rounds.

Key Considerations for Product Managers:

Scalability: Does your AML engine slow down as your user base grows?

Interoperability: Can your compliance data move easily between your KYC provider and your reporting tool?

User Experience: Is your KYC flow so difficult that users abandon the platform?

Is Your Platform Ready?

Navigating OSFI technology risk management Canada and FINTRAC rules requires deep technical expertise. At Espace Info Tech Canada Inc., we specialize in building the secure, audit-ready foundations that Canadian FinTechs need.

Don’t let compliance be an afterthought. Contact Espace Info Tech for a full compliance architecture assessment. We help you build secure, scalable, and audit-ready platforms tailored for the Canadian regulatory environment.